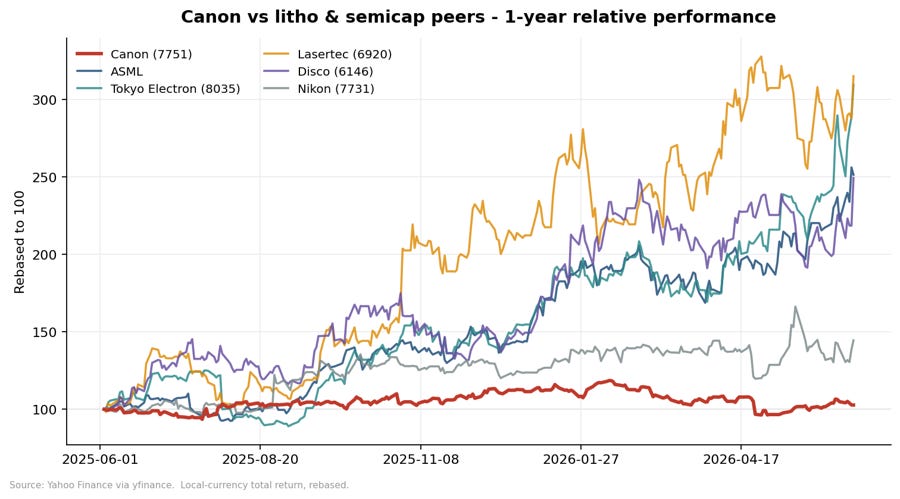

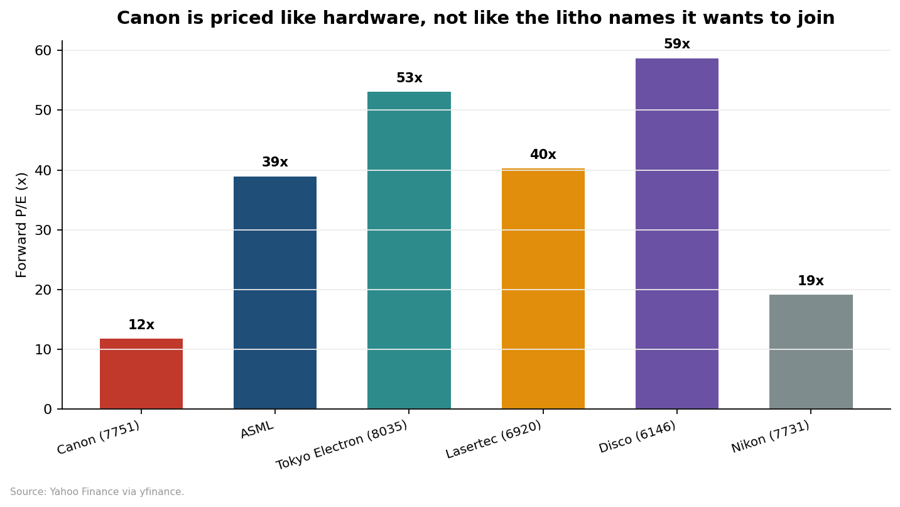

Canon: The Next ASML?

(Written with Xavier Clough)

The Nikkei is up on optimism all is well in the Middle East. The question is what your average foreign investor will focus on now. We suggest it will be legacy value stocks that have underappreciated optionality.

We spent a fair amount of time the other week discussing names that we believe have a long way to run because they are vital to the AI theme. Think 6254 Nomura Micro Sciences. Think 5991 NHK Spring. Think 5384 Fujimi.

We would suggest one of the more interesting laggards is 7751 Canon. And we are also partial to 7912 DNP at these levels.

Canon: The Next ASML?

The headline is obviously doing a lot of heavy lifting. In some ways, it’s outrageous. But let us explain why it’s worth pondering at least.

ASML is the most quietly powerful company in technology. It builds the Extreme Ultraviolet (EUV) lithography machines required to print the world’s most advanced microchips and it is the only company on Earth that can. This absolute monopoly is why leading-edge chipmaking is so scarce, so expensive, and why global governments treat a Dutch toolmaker as vital strategic infrastructure.

A single one of ASML’s High-NA EUV machines costs around $380 million and weighs 165 tons. It operates by blasting molten tin droplets 50,000 times a second with a high-power laser to generate light. That light bounces off mirrors so flawlessly flat that if they were scaled up to the size of Germany, their largest imperfection would be under a millimeter.

No one else can build this. That is exactly why ASML can charge whatever it wants.

So, when asking whether Canon could be the next ASML, the point isn’t that it will dethrone the king next year. The question is narrower and far more compelling: What happens to the company that builds a genuine second pathway to printing advanced chips?

Canon is quietly trying to do exactly that, yet the market continues to price it like a dying camera business.

The Hidden Foundation: Canon is Already a Lithography Titan

Before looking at the disruptive future, consider the profitable reality of today.

The entire global economy runs on enormous volumes of mature-node silicon, the power chips, sensors, and controllers inside everyday electronics. These aren’t cutting-edge chips, and they are printed on older, deep ultraviolet (DUV) lithography tools. Canon has sold these systems for decades. It is a stable, highly profitable business.

Furthermore, the AI era has made “advanced packaging” (stacking multiple chips together) just as important as shrinking individual transistors. This back-end process requires its own specialized lithography. Canon is exceptionally well-positioned in these exact back-end steps, the part of the AI supply chain that scales with every new accelerator and high-bandwidth memory stack yet receives a fraction of the media attention.

The reality is clear: Canon is already an established lithography player. It has simply operated in market niches that Wall Street historically under-valued.

The Asymmetric Swing Factor: Nanoimprint Lithography (NIL)

This is where the thesis gets interesting. Conventional lithography prints using light, firing specific wavelengths through extraordinarily complex optics to project a pattern onto a silicon wafer. Canon’s Nanoimprint Lithography (NIL) completely discards this optical approach.

It prints with a physical stamp.

Because NIL physically presses a master template into a liquid resist on the wafer, like a microscopic printing press, it achieves nanometer-scale features without the massive, power-hungry subsystems that EUV demands.

The economic implications are disruptive:

Keep reading with a 7-day free trial

Subscribe to Kabu Japan to keep reading this post and get 7 days of free access to the full post archives.